Within Fraud Flags

What a fair payment appeal needs

Appeals matter because a blocked transaction is not proof of fraud and customers need fast routes to verify, escalate and correct mistakes.

On this page

- Immediate notices and alternative verification options

- When human support should override automated checks

- Tracking repeat disputes and unresolved customer harm

Page outline Jump by section

Introduction

A blocked payment is not proof of fraud. It is a risk decision, often made partly or wholly by automated systems, and it can be wrong. A fair appeal process should therefore let customers verify themselves quickly, reach human support when the automated check is producing harm, and have repeated mistakes logged so the fraud model and customer process improve. This matters because access to payments is access to ordinary life: rent, wages, travel, bills and business trading can all be affected. UK and European data-protection rules already recognise that significant automated decisions need routes for challenge and human intervention, while financial regulators and ombudsman bodies treat blocked payments and frozen accounts as issues that firms must handle fairly, not merely as back-office security events. [ICO+2Financial Ombudsman]ico.org.ukhose based on profiling, that have a legal or similarly significant effect on…

Fast notice is the first safeguard

A fair appeal starts at the moment the payment is blocked. The customer should be told promptly that the transaction has not gone through, whether any money has been reserved or moved, what action is needed, and how to contact the right team. A vague message such as “transaction declined” leaves the customer guessing whether the issue is fraud screening, insufficient funds, merchant error, sanctions checks, a technical outage or a card limit.

The notice does not need to reveal fraud-detection rules in a way that criminals could exploit. It can still be useful: “We stopped this payment because it looked unusual for your account. Please confirm whether you made it,” gives the customer more practical information than a silent decline. The Financial Ombudsman Service specifically handles complaints about blocked payments and frozen accounts, which shows that the communication around these interruptions is part of the customer harm, not separate from it. [Financial Ombudsman]financial-ombudsman.org.ukFinancial OmbudsmanFrozen accounts and blocked paymentsOn this page you'll discover whether you can bring a complaint about suspended pay…

Good notices should include:

- The transaction affected, including amount, merchant or recipient, and time.

- Whether the customer needs to verify the payment or wait for review.

- A safe route back into the bank or payment provider, such as the official app or a known telephone number.

- A warning not to rely on unexpected inbound calls or messages, because fraudsters often impersonate bank staff.

- An escalation path if the payment is urgent.

That last point is important. Modern payment fraud includes bank-employee impersonation and social-engineering attacks, so the appeal route must avoid creating a new scam opportunity. A bank that sends customers into confusing call-backs or unclear links may solve one fraud problem while creating another. [European Payments Council]europeanpaymentscouncil.euEPC162 24 v2.0 2025 Payments Threats and Fraud Trends ReportEuropean Payments Council2025 Payments Threats and Fraud Trends ReportDecember 1, 2025 — The objective is to trick victims in sharing cre…

Customers need more than one way to verify

Automated fraud systems often flag unusual behaviour: a new device, a large purchase, a new payee, a foreign location, a changed address, or an unfamiliar merchant. Those signals may be sensible risk indicators, but they are also common features of legitimate life. A fair process therefore gives customers several ways to prove that a payment is genuine.

This matters most when the original verification route is unavailable. A customer may have lost a phone, changed number, be travelling, have poor signal, be visually impaired, or be unable to pass a biometric check. If the only appeal route depends on the same device or data point that triggered the block, the customer can become trapped inside the system.

Alternative verification options can include:

- Confirming the transaction inside a secure banking app.

- Speaking to a trained fraud-support agent.

- Repeating authentication through a different factor, such as a passcode or hardware token.

- Verifying a known device or recent account activity.

- Uploading documents through a secure portal where higher-risk review is necessary.

- Using branch or video support for customers who cannot complete digital checks.

The key governance principle is proportionality. A routine false decline should not require the same paperwork as a suspected account takeover. Strong Customer Authentication rules in European payments already reflect this tension: security checks are essential, but payment systems also use risk-based analysis and exemptions to avoid unnecessary friction in lower-risk cases. [European Banking Authority]eba.europa.euEuropean Banking AuthorityOpinion on the implementation of the RTS on SCA and CSC…June 13, 2018 — 13 Jun 2018 — For instance, only the…

Human support must be able to override the machine

An appeal is not meaningful if the human reviewer simply repeats the automated score. Human support should be able to examine context, weigh evidence, recognise urgency, and override the block where appropriate. The UK Information Commissioner’s Office explains that people affected by significant solely automated decisions should have safeguards such as the ability to obtain human intervention, express their view and contest the decision. [ICO]ico.org.ukhose based on profiling, that have a legal or similarly significant effect on…

In blocked-payment appeals, meaningful human review should be available when:

- The payment concerns essentials such as rent, utilities, medical costs, payroll or travel.

- The customer has already verified their identity but remains blocked.

- The same customer has had repeated legitimate payments stopped.

- The blocked payment risks fees, missed obligations or credit-file harm.

- The customer appears vulnerable or unable to navigate the standard digital route.

The human reviewer should not need to expose the fraud model’s full logic to the customer, but they should be able to see enough internal information to make a real decision: the trigger category, the transaction history, previous disputes, verification attempts, account restrictions and any vulnerability notes. The European Data Protection Supervisor has similarly stressed that human oversight of automated decision-making must be effective rather than symbolic. [European Data Protection Supervisor]edps.europa.eu2025 09 23 techdispatch 22025 human oversight automated makingEuropean Data Protection SupervisorTechDispatch #2/2025 - Human Oversight of Automated…by W Wiewiórowski · Cited by 4 — Automated deci…

Appeals should have clear time limits and escalation routes

A blocked payment can become harmful quickly. Delays that look modest from inside a bank can be serious for a customer waiting to pay a deposit, release goods, cover wages or meet a deadline. Fair appeal design should therefore separate low-risk verification, urgent manual escalation and formal complaint handling.

For ordinary verification, the process should aim for minutes, not days. For complex reviews, customers should receive a status update, a reason for delay where legally possible, and a named route for escalation. If the issue becomes a complaint, FCA rules require firms to maintain effective complaint-handling procedures, and consumers can ultimately take eligible unresolved complaints to the Financial Ombudsman Service. [FCA Handbook+2FCA]handbook.fca.org.ukWhere a respondent operates a telephone line for the purpose of enabling an eligible…Read more…

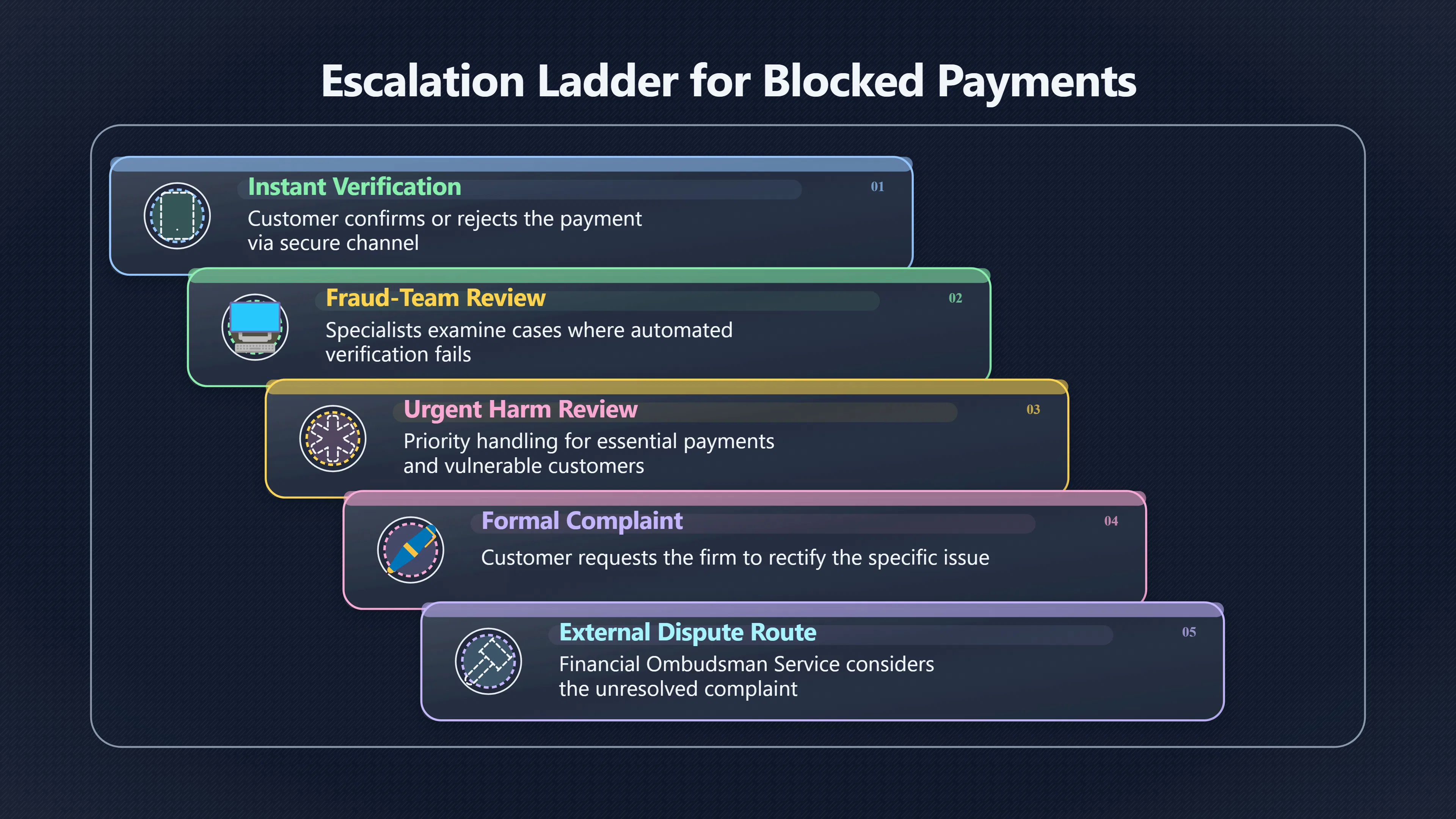

A useful escalation ladder looks like this:

- Instant verification: The customer confirms or rejects the payment through a secure channel.

- Fraud-team review: A specialist reviews cases where automated verification fails.

- Urgent harm review: Essential payments, vulnerable customers and repeated false blocks receive priority.

- Formal complaint: The customer can ask the firm to put things right.

- External dispute route: Where eligible, the Financial Ombudsman Service can consider the complaint.

This structure helps avoid a common failure: treating every blocked payment as either a routine decline or a suspected crime, with no middle path for legitimate customers caught by a risk model.

The hardest cases involve secrecy, safety and fairness at once

Payment providers cannot always explain everything. They may be prevented from disclosing details because of anti-money-laundering duties, sanctions screening, law-enforcement concerns or fraud-risk controls. The FCA’s work on payment account access and closures recognises that firms need effective systems to manage financial-crime and fraud risk, and that those controls may sometimes lead to accounts being suspended, declined or closed. [FCA]fca.org.ukFCAUK Payment Accounts: access and closuresSeptember 20, 2023 — 5 Sept 2023 — This includes effective controls to manage financial crime and fraud risk, which may lead to customers…

But secrecy should not become a blanket excuse for poor treatment. Even where a firm cannot disclose the full reason for a block, it can still explain the process, provide safe contact routes, review evidence, consider customer vulnerability, and avoid leaving people without usable access to funds for longer than necessary. The FCA’s Consumer Duty also pushes firms to consider customer understanding and outcomes across the journey, including communications after account access decisions. [FCA]fca.org.ukFCAUK Payment Accounts Access and Closures: UpdateDuty imposes relevant obligations throughout the customer journey, from a firm's interactions with the…Read more…

The practical test is whether the customer has a real route to resolution. A message that says “we cannot discuss this” may sometimes be legally necessary in part, but a fair process should still answer: what can the customer do, when will the firm review it, and how can urgent harm be raised?

Repeat disputes should feed back into the AI system

Appeals are not just customer-service events. They are evidence about how the fraud-detection system performs in the real world. If customers repeatedly win appeals after the same kind of payment is blocked, the institution has found a model-governance problem, not just a queue-management problem.

Firms should track:

- False-block rates by payment type, channel, merchant category and customer segment.

- Appeal success rates.

- Time taken to restore access.

- Repeat blocks affecting the same customer.

- Complaints involving vulnerable customers. [financial-ombudsman.org.uk]financial-ombudsman.org.ukFinancial OmbudsmanFrozen accounts and blocked paymentsAre you dealing with complaints from customers whose current accounts have been fr…

- Downstream harm, such as missed bills, fees or business disruption.

- Cases where human reviewers frequently override the automated score.

This monitoring should feed into threshold tuning, staff training, customer-message design and model-risk review. The NIST AI Risk Management Framework frames AI risk management as an ongoing process of governing, mapping, measuring and managing risks to people, organisations and society; blocked-payment appeals are a concrete example of that lifecycle in everyday finance. [NIST Publications]nvlpubs.nist.govNIST PublicationsArtificial Intelligence Risk Management Framework (AI RMF 1.0)June 4, 2025 — by N AI · 2023 · Cited by 228 — NIST plans…

Unresolved harm should be treated as part of the error

A payment block is not fully corrected just because the transaction is later approved. The customer may already have missed a deadline, lost a purchase, incurred fees, damaged a supplier relationship or been left without money at a critical moment. Fair appeals should therefore ask not only “was the payment genuine?” but also “what happened because we blocked it?”

The Financial Ombudsman Service’s published material on blocked payments and frozen accounts makes clear that complaints can involve the way a firm handled the block, not only whether the firm had any reason to act. In one ombudsman decision involving blocked and closed accounts, the complaint included concern that the customer had missed a loan payment because of the block. [Financial Ombudsman]financial-ombudsman.org.ukFinancial OmbudsmanFrozen accounts and blocked paymentsOn this page you'll discover whether you can bring a complaint about suspended pay…

That distinction matters for AI governance. A fraud model may be statistically defensible overall while still causing avoidable harm in particular cases. Recording downstream consequences gives firms a better view of the real cost of false positives and helps prevent “accuracy” from being defined only in technical terms.

What a fair blocked-payment appeal needs

A fair payment appeal should be fast, understandable, multi-channel and capable of changing the outcome. It should respect the genuine need to stop fraud while recognising that a blocked transaction is only a suspicion. The strongest systems combine security controls with customer safeguards:

- Immediate, safe notice when a payment is blocked.

- Clear verification options that do not depend on a single device or channel.

- Human reviewers with authority to override automated checks.

- Priority handling for urgent, repeated or vulnerable-customer cases.

- Complaint and ombudsman routes where internal review fails.

- Feedback loops that use successful appeals to improve the model and process.

- Tracking of unresolved harm, not just final approval or decline status.

This is where blocked-payment appeals become part of understanding artificial intelligence. The fairness of an AI-assisted fraud system is not measured only by how quickly it detects suspicious activity. It is also measured by how well it corrects mistakes when legitimate customers are wrongly stopped from using their own money.

Amazon book picks

Further Reading

Books and field guides related to What a fair payment appeal needs. Use these as the next step if you want deeper reading beyond the article.

The Power of Customer Experience

Explains fair treatment, complaints handling, customer journeys, and organisational responses when systems cause harm.

Co-Intelligence

Helps readers understand when human review should complement automated decisions.

Weapons of Math Destruction

Directly addresses unfair automated decisions, accountability, and appeals.

The Alignment Problem

Explores how machine-learning systems can create unintended outcomes and how institutions respond.

eBay marketplace picks

Marketplace Samples

Example marketplace items related to this page. Use the search link to explore similar finds on eBay.

![Listing image for [Lot] New World Aeternum Developer Exclusive Artbook / Desk Mat / Steelbook Game](/assets/images/marketplace-covers/4262455386b429ab533b.jpg)

Endnotes

-

Source: ico.org.uk

Link: https://ico.org.uk/for-organisations/uk-gdpr-guidance-and-resources/individual-rights/individual-rights/rights-related-to-automated-decision-making-including-profiling/Source snippet

hose based on profiling, that have a legal or similarly significant effect on...

-

Source: ico.org.uk

Link: https://ico.org.uk/for-the-public/your-rights-relating-to-decisions-being-made-about-you-without-human-involvement/Source snippet

Your rights relating to decisions being made about you...Organisations must not make decisions based solely on automated processing if t...

-

Source: fca.org.uk

Title: how complain

Link: https://www.fca.org.uk/consumers/how-complainSource snippet

How to complain17 Apr 2016 — If you're unhappy with a financial product or service, get in touch with the firm. Tell them what happened a...

-

Source: nvlpubs.nist.gov

Link: https://nvlpubs.nist.gov/nistpubs/ai/nist.ai.100-1.pdfSource snippet

NIST PublicationsArtificial Intelligence Risk Management Framework (AI RMF 1.0)June 4, 2025 — by N AI · 2023 · Cited by 228 — NIST plans...

Published: June 4, 2025

-

Source: nist.gov

Link: https://www.nist.gov/itl/ai-risk-management-frameworkSource snippet

iated with artificial intelligence (AI)...

-

Source: clear.sale

Title: Everything You Need to Know About False Declines

Link: https://www.clear.sale/blog/everything-you-need-to-know-about-false-declinesSource snippet

SaleLearn about false declines, including strategies for reducing false declines to enhance customer experience and safeguard revenue...

-

Source: financial-ombudsman.org.uk

Link: https://www.financial-ombudsman.org.uk/consumers/complaints-can-help/banking-and-payments/frozen-accounts-blocked-paymentsSource snippet

Financial OmbudsmanFrozen accounts and blocked paymentsOn this page you'll discover whether you can bring a complaint about suspended pay...

-

Source: financial-ombudsman.org.uk

Link: https://www.financial-ombudsman.org.uk/businesses/complaints-deal/banking-and-payments/frozen-accounts-blocked-paymentsSource snippet

Financial OmbudsmanFrozen accounts and blocked paymentsAre you dealing with complaints from customers whose current accounts have been fr...

-

Source: europeanpaymentscouncil.eu

Title: EPC162 24 v2.0 2025 Payments Threats and Fraud Trends Report

Link: https://www.europeanpaymentscouncil.eu/sites/default/files/kb/file/2026-02/EPC162-24%20v2.0%202025%20Payments%20Threats%20and%20Fraud%20Trends%20Report.pdfSource snippet

European Payments Council2025 Payments Threats and Fraud Trends ReportDecember 1, 2025 — The objective is to trick victims in sharing cre...

Published: December 1, 2025

-

Source: eba.europa.eu

Link: https://www.eba.europa.eu/sites/default/files/documents/10180/2137845/0f525dc7-0f97-4be7-9ad7-800723365b8e/Opinion%20on%20the%20implementation%20of%20the%20RTS%20on%20SCA%20and%20CSC%20%28EBA-2018-Op-04%29.pdfSource snippet

European Banking AuthorityOpinion on the implementation of the RTS on SCA and CSC...June 13, 2018 — 13 Jun 2018 — For instance, only the...

Published: June 13, 2018

-

Source: eba.europa.eu

Title: eba publishes opinion elements strong customer authentication

Link: https://www.eba.europa.eu/publications-and-media/press-releases/eba-publishes-opinion-elements-strong-customer-authenticationSource snippet

European Banking AuthorityEBA publishes an Opinion on the elements of strong customer...21 Jun 2019 — The European Banking Authority (EB...

-

Source: edps.europa.eu

Title: 2025 09 23 techdispatch 22025 human oversight automated making

Link: https://www.edps.europa.eu/data-protection/our-work/publications/techdispatch/2025-09-23-techdispatch-22025-human-oversight-automated-makingSource snippet

European Data Protection SupervisorTechDispatch #2/2025 - Human Oversight of Automated...by W Wiewiórowski · Cited by 4 — Automated deci...

-

Source: handbook.fca.org.uk

Link: https://handbook.fca.org.uk/handbook/disp1/disp1s3Source snippet

Where a respondent operates a telephone line for the purpose of enabling an eligible...Read more...

-

Source: fca.org.uk

Title: FCAUK Payment Accounts: access and closures

Link: https://www.fca.org.uk/publication/corporate/uk-payment-accounts-access-and-closures.pdfSource snippet

September 20, 2023 — 5 Sept 2023 — This includes effective controls to manage financial crime and fraud risk, which may lead to customers...

Published: September 20, 2023

-

Source: fca.org.uk

Title: FCAUK Payment Accounts Access and Closures: Update

Link: https://www.fca.org.uk/publication/corporate/uk-payment-accounts-access-closures-update.pdfSource snippet

Duty imposes relevant obligations throughout the customer journey, from a firm's interactions with the...Read more...

-

Source: fca.org.uk

Title: uk payment accounts access and closures update

Link: https://www.fca.org.uk/publications/corporate-documents/uk-payment-accounts-access-and-closures-updateSource snippet

UK payment accounts access and closures: updateSep 4, 2024 — This report follows on from our 2023 report, UK Payment Accounts: access and...

-

Source: financial-ombudsman.org.uk

Title: DRN 2773561

Link: https://www.financial-ombudsman.org.uk/decision/DRN-2773561.pdfSource snippet

Decision Reference DRN-2773561Mr J complained to the bank about his accounts being blocked and then closed. Mr J felt he'd been unfairly...

-

Source: fca.org.uk

Link: https://www.fca.org.uk/consumers/fraudulent-payments -

Source: fca.org.uk

Title: anti fraud controls complaint handling firms focus app fraud

Link: https://www.fca.org.uk/publications/multi-firm-reviews/anti-fraud-controls-complaint-handling-firms-focus-app-fraudSource snippet

Anti-fraud controls and complaint handling in firms (with a...7 Nov 2023 — This publication sets out the key findings from our review of...

-

Source: fca.org.uk

Link: https://www.fca.org.uk/firms/financial-crime/fraudSource snippet

22 Feb 2016 — Fraud falls within the FCA's objective of reducing the risk of financial crime and also affects our consumer protection obj...

-

Source: fca.org.uk

Title: banks fraud controls comparison

Link: https://www.fca.org.uk/data/banks-fraud-controls-comparisonSource snippet

Comparison of banking providers' fraud controls9 Mar 2020 — Real-time fraud detection Our systems are designed to detect fraudulent payme...

-

Source: fca.org.uk

Title: complaints handling review findings

Link: https://www.fca.org.uk/publications/multi-firm-reviews/complaints-handling-review-findingsSource snippet

15 Aug 2018 — The findings of our review of how Non-deposit Taking Mortgage Lenders (NDTMLs) and Mortgage Third-Party Administrators (MTP...

-

Source: fca.org.uk

Title: uk payment accounts access and closures

Link: https://www.fca.org.uk/publications/corporate-documents/uk-payment-accounts-access-and-closuresSource snippet

UK Payment Accounts: access and closuresSep 19, 2023 — We set out key insights from our work on the provision of payment accounts to pers...

-

Source: financial-ombudsman.org.uk

Link: https://www.financial-ombudsman.org.uk/consumers/complaints-can-help/banking-and-paymentsSource snippet

Banking and paymentsFrozen accounts and blocked payments Do you have a complaint about the way your bank or building society froze your a...

-

Source: financial-ombudsman.org.uk

Link: https://www.financial-ombudsman.org.uk/businesses/complaints-deal/banking-and-payments/bank-account-closuresSource snippet

Bank account closuresDo you deal with customer complaints about bank account closures? This page will give you an overview of the complai...

-

Source: eba.europa.eu

Link: https://www.eba.europa.eu/regulation-and-policy/consumer-protectionSource snippet

protection | European Banking AuthorityThe EBA identifies and addresses harm that arises for EU consumers as a result of their interactio...

-

Source: witness.ai

Title: ai risk management

Link: https://witness.ai/blog/ai-risk-management/Source snippet

NIST AI RMF & Key Strategies13 Nov 2025 — Discover what AI risk management is, why it matters, and how to apply the NIST AI RMF with gove...

-

Source: GOV.UK

Link: https://www.gov.uk/government/publications/recommendations-on-payments-regulation-for-the-financial-conduct-authority-and-payment-systems-regulator-november-2024/joint-response-from-the-financial-conduct-authority-and-the-payment-systems-regulatorSource snippet

response from the Financial Conduct Authority and...16 Dec 2025 — The PSR has commissioned an independent review of its APP scams polici...

Additional References

-

Source: psr.org.uk

Link: https://www.psr.org.uk/information-for-consumers/app-fraud-reimbursement-protections/Source snippet

APP fraud reimbursement protectionsAuthorised Push Payment (APP) fraud is a devastating crime. These protections start on 7 October 2024...

Published: October 2024

-

Source: gdpr-info.eu

Link: https://gdpr-info.eu/art-22-gdpr/Source snippet

Automated individual decision-making, including profilingThe data subject shall have the right not to be subject to a decision based sole...

-

Source: citizensadvice.org.uk

Link: https://www.citizensadvice.org.uk/debt-and-money/banking/complaints-about-banks-and-building-societies/Source snippet

Complaints about banks and building societiesYou can also contact the Financial Ombudsman Service's consumer helpline on 0800 023 4 567 o...

-

Source: addleshawgoddard.com

Link: https://www.addleshawgoddard.com/en/insights/insights-briefings/2024/financial-regulation/financial-regulation-in-the-know-payments-september-2024/fca-follow-up-report-uk-payment-accounts-access-closures/Source snippet

FCA follow-up Report: UK Payment Accounts Access and...Clear and Comprehensive Communication with Customers: In instances where access t...

-

Source: gocardless.com

Link: https://gocardless.com/en-au/guides/posts/how-to-prevent-false-declines-in-ecommerce/Source snippet

How to Prevent False Declines in EcommerceReducing false declines · Upgrade your fraud protection tools. Legitimate transactions being er...

-

Source: avolutionsoftware.com

Link: https://www.avolutionsoftware.com/our-resources/nist-ai-risk-management-framework-rmf/Source snippet

NIST AI Risk Management Framework (RMF)The NIST AI Risk Management Framework, often called the NIST AI RMF, gives organizations a practic...

-

Source: epic.org

Link: https://epic.org/documents/epic-comments-national-institute-of-standards-and-technology-ai-risk-management-framework/Source snippet

National Institute of Standards and Technology AI Risk...EPIC believes the AI RMF is most effective where it provides clear directions o...

-

Source: psr.org.uk

Link: https://www.psr.org.uk/media/rhelv4op/ps25-5-app-scams-reimbursement-consolidated-policy-statement-may-2025.pdfSource snippet

PS25/5 APP scams reimbursement requirement...Fighting authorised push payment fraud: That requirement came into effect on 7 October 2024...

Published: October 2024

-

Source: linkedin.com

Link: https://www.linkedin.com/posts/neirajones_the-story-so-far-a-snapshot-of-what-weve-activity-7328717829631873024-anBrSource snippet

PSR's new rules reduce APP scams in UKThe Payment Systems Regulator #PSR published its Authorised Push Payment Scams Reimbursement Dashbo...

-

Source: dnb.nl

Link: https://www.dnb.nl/en/contact/reporting-complaints-and-wrongdoing/complaints-about-institutions/Source snippet

Reporting complaints and wrongdoingContact us if you have complaints about financial institutions. You can also report any actual or susp...

Topic Tree